Leyland Lines - July Insights

Welcome to the July edition of our newsletter for 2022.

Markets went up 4% in July, following a weak end to the 2022 financial year. Volume in the market has been very low, as investors await reporting season to ascertain the impact of rising labour, energy and funding costs.

For the first time in 10 years or more inflation, rising interest rates and how central banks will implement policy in relation to these factors are in play

Regarding the consumer, the following appear favourable:

- High levels of household equity (excl. more recent 1st home buyers)

- Tight labour market placing upward pressure on incomes

- Reasonably low levels of consumer leverage (excl. more recent 1st home buyers)

- Strong household savings accumulated during the pandemic

As with anything in economics there is a balance, and the following factors will adversely impact the consumer:

- Inflationary pressures, including non-discretionary items such as energy and food

- Income rises not keeping pace with inflation (spending power reducing)

- Falling home prices, negatively affecting sentiment

- Central banks attempting to impact spending through tight monetary policy (raising rates)

- Increasing likelihood of a recession (if not already here)

Some of the key inputs impacting inflation appear to be moderating, as you may have experienced more recently while filling up your vehicle at the bouser.

Another example is global container shipping costs, which have come down.

Central bank policies are driving markets at the moment. Reporting season commences next month, which will provide us the opportunity to see the impact of inflationary pressures on earnings.

In this edition of Leyland Lines, we discuss Treasury Wine Estates Limited as a stock to watch. We also consider some of our key takeaways for making better decisions after reading Annie Duke’s book “Thinking in Bets”. For the video of the month, we include Alex Leyland’s chat with the Ausbiz team. Finally, as a reminder of Buffett’s timeless wisdom we include his 2020 letter to Berkshire Hathaway shareholders.

Video of the Month

How reliable are RBA forecasts

Alex Leyland discusses the (in)accuracy of RBA forecasts

Treasury Wine Estates Limited

(ASX: TWE)

Share Price: $12.21

Market Cap: $8.6b

A Brief Description and History of Treasury Wine Estates

Treasury Wine Estates (TWE) has a global team of over 2,600 people and is listed on the Australian Securities Exchange (ASX) with a market capitalisation of around $AUD8.5Billlion, which has grown from $2.2bn since listing in May 2011.

TWE sees itself as the custodian of some of the world’s most trusted premium wine brands, creating long-term value by being sustainable in everything it does.

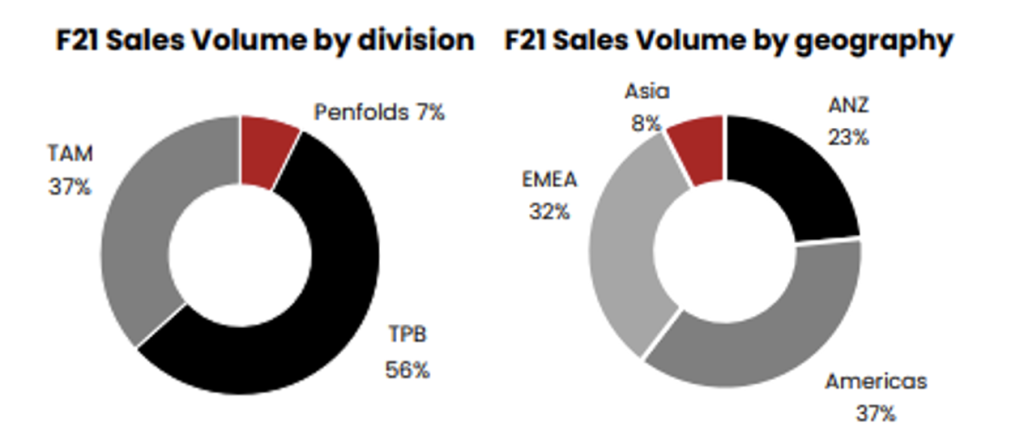

TWE’s global distribution platform, which features competitively advantaged and differentiated routes to market, supports sales in over 70 countries across three standalone brand portfolio divisions:

- Penfolds,

- Treasury Premium Brands (TPB)

- Treasury Americas (TAM).

Supporting the brand portfolio divisions are the Supply, Treasury Business Solutions and Corporate functions, key enablers to ensuring TWE leverages the scale of its global business model.

At the heart of the business is TWE’s global, multi-regional sourcing model which includes world class vineyard and production assets in internationally acclaimed wine-making regions including the Barossa Valley in Australia, the Napa Valley in the United States, Marlborough in New Zealand, Bordeaux in France and Tuscany in Italy.

Luxury and Premium brands now represent over 80% of global revenue for TWE, up from less than 50% in 2015.

TWE’s long-term investment case comprises five key elements that it expects to drive future performance and the delivery of TWE’s long-term Group EBIT margin target of +25%:

Attractive premium wine category fundamentals, with growing premium wine consumption continuing to drive category volume and value growth across all key markets.

An unrivalled portfolio of well-known and trusted premium wine brands spanning consumer tastes, consumption occasions and price points.

Competitively advantaged and differentiated route-to-market models that provide a global, multi-channel distribution platform which is unrivalled in the wine industry.

World class vineyard and production assets in internationally acclaimed wine making regions, reflecting a truly global, diversified multi-regional sourcing model, and

A strong, flexible and efficient capital structure, supporting investment for future growth and the ongoing delivery of returns for TWE’s shareholders.

The successful execution of TWE’s corporate strategy is reflected in the performance of the Group across its key financial metrics.

A few key Numbers:

| Revenue | 2.6bil | 2.5bil | 2.7bil | 2.8bil |

| Net Profit after Tax | 316m | 330m | 410m | 465m |

| Price Earnings Ratio | 25 | 24 | 19 | 17 |

| Dividend Yield % | 2.5 | 3 | 3.5 | 4 |

Source: TWE, FactSet

A few key dates:

1843. Lindeman’s Vineyard established in The Hunter Valley NSW.

1844. Penfolds wine established on the outskirts of Adelaide by Dr Christopher Rawson Penfold and his wife Mary.

1985. Penfolds buys Allied Vintners Group, which includes Wynns Coonawarra Estate.

1994. Penfolds Wine Group renamed Southcorp.

2001. Southcorp acquires Matua Valley (NZ). Southcorp and Rosemount Estate merge to become Australia’ largest wine company.

2005. Foster’s Group acquires Southcorp and combines it with its existing wine business, Beringer Blass from the Napa Valley.

2011. Foster’s Group renames the wine business, Treasury Wine Estates, de-merges and lists it separately on the ASX on 9th of May 2011.

2014 to 2020. Treasury wine buys significant wine producing assets in California and France and dramatically improves its distribution channels.

2021. Treasury Wine Estates transitions to the new operating model mentioned earlier with the three main divisions. Penfolds, Treasury Premium Brands and Treasury Americas.

TWE has more than 40 famous and iconic brand names, most of which are household names. Below are pictured just a few.

A few recent developments and thoughts on TWE.

China Issues

The price chart above shows that the TWE share price sold off with the rest of the market around the time of the Covid outbreak. TWE’s share price did not fully recover with most other stocks, primarily due to the Chinese Government imposing prohibitive taxes on Australian wine.

Through good management, TWE has been able to replace China sales with sales to other regions.

However, there is still a dramatic ‘blue sky’ potential catalyst for TWE in the form of expansion into China from Treasury Premium Brands (TPB) and scope for a potential Chinese Penfolds product, as has been recently speculated in the press (Chinese Penfolds), via blending wines from Ningxia and South Australia.

Industry Data

The latest Nielsen US wine industry data highlights the ongoing volume declines and price realisation. The total sales year on year for the four weeks to 18th June 2022 showed a decline of 2.8%. Interestingly, on a 3-year basis industry sales are up 3.4%, despite a flat volume. This data reflects US retail channels and Treasury wines has had a slightly worse decline in their sales numbers to retail.

The priority brands have exhibited mixed performance with some brands down 6% for the last 12 months and some up as much 17% per annum for the last 3 years. Comparisons of this nature can be misleading as they can follow weak and/or strong previous periods. Nevertheless, the outstanding TWE growth brands, at the moment, are Matua from NZ and Franks Family Vineyard in the US.

Whilst, TWE has had reduction in its market share to industry, this has been offset by price realisation. Some examples of price growth in their brands are: 19 Crimes 3.6%, Lindemans 8%, Matua 2.6% and Stag’s Leap 2.6%.

TWE sales in the US are ahead of pre-Covid but behind industry growth, (partly due to a commercial wine divestment in March 21) 19 crimes represents 40% of total sales in the US.

Treasury Premium Brands, potential good news

Recently Treasury Premium Brands (TPB) MD, Peter Neilsen suggested in an interview with Jarden that there are 5 potential drivers for TPB to be a surprise growth leader for Treasury Estate Wines.

-

- Global penetration: Outside of core markets, notably in the EU/Asia, as well as non-alcoholic/low-alcohol wine.

- Brand expansion: Via brand stretch (i.e. Rawson’s South Africa and Argentina), and premiumisation, (Wynn’s) and new brands.

- Easing Costs, (COGS) into 2022 going lower as well as other efficiencies in its wineries.

- Leveraging scale to win share of shelf with retail partners that are increasingly looking to deal with fewer suppliers that offer more range and volume. This should particularly benefit TWE in less penetrated markets.

- Channel normalisation in a global reopening will improve margins via a return of materially higher margin, travel, cellar door and on-premise sales.

Signs from competitors augur well.

Duckhorn’s, a significant, listed US competitor, in its April 2022 quarter result revealed a continued recovery in the higher-margin on-premise and cellar door channels and resilience in the off-premises channel, which is consistent with recent read-throughs from industry peers (Pernod and Constellation). The improvement in Duckhorn’s on-premises sales supports the view that Treasury Americas’ guidance of 2H22 trading conditions remaining similar to 1H22, could be too conservative.

Duckhorn indicated the recovery continued in the on-premise channel with growth accelerating on a 3-year CAGR basis on all three key metrics – cases, accounts sold and points of distribution.

Duckhorn’s ‘wholesale to distributor’ channel grew by 5.5% during 3Q22 (April ending) on the pcp as on-premise continued to grow faster than off-premise. The California direct-to-retail channel also increased 7% on the pcp driven by strength in on-premise. All this is a positive read through for Treasury Wine Estates.

Lastly, Constellation Brands’, another significant competitor, 4Q22 result (ending 28 Feb 22) revealed inflationary pressures adversely impacted earnings, with cost headwinds likely to continue in FY23 (ending Feb 23). This is consistent with cost pressures flagged by Treasury at its Feb 22 result. Based on the Constellation result it is unknown whether the A$5 million to A$10 million headwind relating to 2H22 packaging costs that Treasury flagged at its 1H22 result will be sufficient. Nonetheless, cost pressures Treasury is facing should be offset by price rises of popular wine brands (Constellation also doing this), premiumisation and re-opening of higher margin on premise channels.

TWE believes, based on its experience from previous recessions, consumers continue to spend on alcohol although they may pause larger purchases as this is a small luxury they still want to experience.

And just for fun, Penfolds is launching a Non fungible token (NFT)

In November 2021, Treasury Wine was in the headlines with news its Penfolds brand is partnering with Blockbar to produce NFTs. According to Penfolds, Blockbar is a leading NFT marketplace for luxury wines and spirits. The platform’s users will be able to purchase a limited edition NFT tied to a rare barrel of Penfolds Magill Cellar 3 wine.

The barrel contains vintage 2021 and is available for purchase for US$130,000, payable in either Ethereum (CYRPTO: ETH), credit card, or wire transfer. The single barrel NFT will be converted into 300 bottle NFTs when the wine is bottled in October 2022. Those bottle NFTs will then be able to be swapped for a physical bottle in October 2023.

Each bottle will be stored at BlockBar’s facility until its purchaser redeems their NFT. Additionally, whoever owns the barrel NFT at the time of bottling will get a personalised barrel head. They will also be able to participate in some special experiences.

If you are unsure what this means, you are not alone, however it seems if digital currencies take off again, then TWE will be there riding on the coat tails.

In summary, TWE is building toward a favourable medium-term operating setting. This contrasts to the last few difficult years which have been well-handled by management, all things considered. The favourable outlook is against relatively low market expectations. This is particularly so if TWE can demonstrate pricing power and benefit from a global reopening.

Sources. Google, Treasury Wine Estates, JP

Morgan, Jarden, Citi, Motley Fool

Tony Barry

Reviewing Annie Duke’s Thinking in Bets

A prerequisite to good investing involves understanding the game you are playing. Unsurprisingly, a major component of successful investing revolves around how to analyse a company. But equally important is the psychological wiring of the investor. In many respects, the share market is one of the great tests of one’s psychology and their predisposition to the many behavioural biases that impact decision making. In search of making better (life) decisions (and hopefully, better investment decisions) I recently read Annie Duke’s “Thinking in Bets”. Psychologist by training, Duke reflects on getting comfortable with uncertainty and provides mechanisms for making better decisions as a result. She weaves these lessons while taking the reader through her journey from being a poker novice to becoming a World Series of Poker champion. In this piece, I discuss how investing is in many respects more similar to poker than chess. I also cover why we should focus on the process and not the outcome. In next month’s newsletter I will continue the journey into decision-making and share tips directed at enhancing our decision-making processes.

Life is Poker, not Chess

You may be wondering why Duke’s journey through poker tournaments is remotely relevant to investing. There is of course the obvious point that some investors (or more appropriately, speculators) treat the share market like a casino. Leaving that parallel to one side, there is a deeper connection between poker and investing. The notion behind the book and its titling “Thinking in bets” is that our lives are determined by two factors: 1.) the quality of our decisions and 2.) luck.

Poker shares a similarity to life in this respect, both luck and the quality of decision-making influence a player’s success. This contrasts with the game of chess, where 99 times out of 100 the more skilled (not the luckier) player will win. Per Duke “Chess, for all its strategic complexity, isn’t a great model for decision-making in life, where most of our decisions involve hidden info and a much greater influence of luck. Poker, in contrast, is a game of incomplete information. It is a game of decision-making under conditions of uncertainty over time. There is also an element of luck in any outcome.”

Poker and investing are similar in how luck can influence the outcome. Investing is one of the few disciplines where an amateur can beat a professional, purely by getting lucky on the stock they choose to invest in. One could conceivably plot activities on a continuum of “luck” and “skill”. On the one side, pursuits like basketball and chess would sit closer to the “skill” end of the continuum. I can’t envision myself defeating Lebron James in basketball, irrespective of how lucky I may be on the day. On the other extreme, games like roulette would sit on the “luck” end of the continuum. To know how much of a factor luck has on a game’s outcome, academic, Michael Mauboussin suggests thinking about whether you can lose the game on purpose. Those instances where you can, point to the greater influence of skill.

Focus on the process not the outcome

Importantly, while we cannot influence the role of luck, we can enhance the quality of our decision making. Pitting the professional investor against the amateur, in answering who will outperform in the long run, my money is on the one with the better decision-making process.

Duke points out that it is unwise to draw an overly tight relationship between results and decision quality. More specifically, we are better served focusing on the decision (and more importantly, the decision-making process) not the result because the influence of luck on outcomes. Hindsight bias – the tendency, after an outcome is known to see the outcome as being inevitable – is relevant here and points to some of the dangers of focusing on outcomes and not the process. Per Duke “outcomes don’t tell us what’s our fault and what isn’t, what we should take credit for and what we shouldn’t. Unlike in chess, we can’t simply work backward from the quality of the outcome to determine the quality of our beliefs or decisions”.

It is human nature to be uncomfortable with the idea that luck plays an outsized role in our lives. However, the sooner we become conscious of the role of luck, the sooner we can take steps to make better decisions. In next month’s newsletter I will unpack practical steps on improving our decision-making processes.

Kiefer de Silva

Berkshire Hathaway 2020 Annual Letter

To the Shareholders of Berkshire Hathaway Inc.:

Berkshire earned $42.5 billion in 2020 according to generally accepted accounting principles (commonly called “GAAP”). The four components of that figure are $21.9 billion of operating earnings, $4.9 billion of realized capital gains, a $26.7 billion gain from an increase in the amount of net unrealized capital gains that exist in the stocks we hold and, finally, an $11 billion loss from a write-down in the value of a few subsidiary and affiliate businesses that we own. All items are stated on an after-tax basis.

Operating earnings are what count most, even during periods when they are not the largest item in our GAAP total. Our focus at Berkshire is both to increase this segment of our income and to acquire large and favorably-situated businesses. Last year, however, we met neither goal: Berkshire made no sizable acquisitions and operating earnings fell 9%. We did, though, increase Berkshire’s per-share intrinsic value by both retaining earnings and repurchasing about 5% of our shares.

The two GAAP components pertaining to capital gains or losses (whether realized or unrealized) fluctuate capriciously from year to year, reflecting swings in the stock market. Whatever today’s figures, Charlie Munger, my long-time partner, and I firmly believe that, over time, Berkshire’s capital gains from its investment holdings will be substantial.

As I’ve emphasized many times, Charlie and I view Berkshire’s holdings of marketable stocks – at yearend worth $281 billion – as a collection of businesses. We don’t control the operations of those companies, but we do share proportionately in their long-term prosperity. From an accounting standpoint, however, our portion of their earnings is not included in Berkshire’s income. Instead, only what these investees pay us in dividends is recorded on our books. Under GAAP, the huge sums that investees retain on our behalf become invisible.

What’s out of sight, however, should not be out of mind: Those unrecorded retained earnings are usually building value – lots of value – for Berkshire. Investees use the withheld funds to expand their business, make acquisitions, pay off debt and, often, to repurchase their stock (an act that increases our share of their future earnings). As we pointed out in these pages last year, retained earnings have propelled American business throughout our country’s history. What worked for Carnegie and Rockefeller has, over the years, worked its magic for millions of shareholders as well.

Of course, some of our investees will disappoint, adding little, if anything, to the value of their company by retaining earnings. But others will over-deliver, a few spectacularly. In aggregate, we expect our share of the huge pile of earnings retained by Berkshire’s non-controlled businesses (what others would label our equity portfolio) to eventually deliver us an equal or greater amount of capital gains. Over our 56-year tenure, that expectation has been met.

The final component in our GAAP figure – that ugly $11 billion write-down – is almost entirely the quantification of a mistake I made in 2016. That year, Berkshire purchased Precision Castparts (“PCC”), and I paid too much for the company.

No one misled me in any way – I was simply too optimistic about PCC’s normalized profit potential. Last year, my miscalculation was laid bare by adverse developments throughout the aerospace industry, PCC’s most important source of customers.

In purchasing PCC, Berkshire bought a fine company – the best in its business. Mark Donegan, PCC’s CEO, is a passionate manager who consistently pours the same energy into the business that he did before we purchased it. We are lucky to have him running things.

I believe I was right in concluding that PCC would, over time, earn good returns on the net tangible assets deployed in its operations. I was wrong, however, in judging the average amount of future earnings and, consequently, wrong in my calculation of the proper price to pay for the business. PCC is far from my first error of that sort. But it’s a big one.

Two Strings to Our Bow

Berkshire is often labeled a conglomerate, a negative term applied to holding companies that own ahodge-podge of unrelated businesses. And, yes, that describes Berkshire – but only in part. To understand how and why we differ from the prototype conglomerate, let’s review a little history.

Over time, conglomerates have generally limited themselves to buying businesses in their entirety. That strategy, however, came with two major problems. One was unsolvable: Most of the truly great businesses had no interest in having anyone take them over. Consequently, deal-hungry conglomerateurs had to focus on so-so companies that lacked important and durable competitive strengths. That was not a great pond in which to fish.

Beyond that, as conglomerateurs dipped into this universe of mediocre businesses, they often found themselves required to pay staggering “control” premiums to snare their quarry. Aspiring conglomerateurs knew the answer to this “overpayment” problem: They simply needed to manufacture a vastly overvalued stock of their own that could be used as a “currency” for pricey acquisitions. (“I’ll pay you $10,000 for your dog by giving you two of my $5,000 cats.”)

Often, the tools for fostering the overvaluation of a conglomerate’s stock involved promotional techniques and “imaginative” accounting maneuvers that were, at best, deceptive and that sometimes crossed the line into fraud. When these tricks were “successful,” the conglomerate pushed its own stock to, say, 3x its business value in order to offer the target 2x its value.

Investing illusions can continue for a surprisingly long time. Wall Street loves the fees that deal-making generates, and the press loves the stories that colorful promoters provide. At a point, also, the soaring price of a promoted stock can itself become the “proof” that an illusion is reality.

Eventually, of course, the party ends, and many business “emperors” are found to have no clothes. Financial history is replete with the names of famous conglomerateurs who were initially lionized as business geniuses by journalists, analysts and investment bankers, but whose creations ended up as business junkyards.

Conglomerates earned their terrible reputation.

* * * * * * * * * * * *

Charlie and I want our conglomerate to own all or part of a diverse group of businesses with good economic characteristics and good managers. Whether Berkshire controls these businesses, however, is unimportant to us.

It took me a while to wise up. But Charlie – and also my 20-year struggle with the textile operation I inherited at Berkshire – finally convinced me that owning a non-controlling portion of a wonderful business is more profitable, more enjoyable and far less work than struggling with 100% of a marginal enterprise.

For those reasons, our conglomerate will remain a collection of controlled and non-controlled businesses. Charlie and I will simply deploy your capital into whatever we believe makes the most sense, based on a company’s durable competitive strengths, the capabilities and character of its management, and price.

If that strategy requires little or no effort on our part, so much the better. In contrast to the scoring system utilized in diving competitions, you are awarded no points in business endeavors for “degree of difficulty.” Furthermore, as Ronald Reagan cautioned: “It’s said that hard work never killed anyone, but I say why take the chance?”

The Family Jewels and How We Increase Your Share of These Gems

On page A-1 we list Berkshire’s subsidiaries, a smorgasbord of businesses employing 360,000 at yearend. You can read much more about these controlled operations in the 10-K that fills the back part of this report. Our major positions in companies that we partly own and don’t control are listed on page 7 of this letter. That portfolio of businesses, too, is large and diverse.

Most of Berkshire’s value, however, resides in four businesses, three controlled and one in which we have only a 5.4% interest. All four are jewels. The largest in value is our property/casualty insurance operation, which for 53 years has been the core of Berkshire. Our family of insurers is unique in the insurance field. So, too, is its manager, Ajit Jain, who joined Berkshire in 1986.

Overall, the insurance fleet operates with far more capital than is deployed by any of its competitors worldwide. That financial strength, coupled with the huge flow of cash Berkshire annually receives from its non-insurance businesses, allows our insurance companies to safely follow an equity-heavy investment strategy not feasible for the overwhelming majority of insurers. Those competitors, for both regulatory and credit-rating reasons, must focus on bonds.

And bonds are not the place to be these days. Can you believe that the income recently available from a 10-year U.S. Treasury bond – the yield was 0.93% at yearend – had fallen 94% from the 15.8% yield available in September 1981? In certain large and important countries, such as Germany and Japan, investors earn a negative return on trillions of dollars of sovereign debt. Fixed-income investors worldwide – whether pension funds, insurance companies or retirees – face a bleak future.

Some insurers, as well as other bond investors, may try to juice the pathetic returns now available by shifting their purchases to obligations backed by shaky borrowers. Risky loans, however, are not the answer to inadequate interest rates. Three decades ago, the once-mighty savings and loan industry destroyed itself, partly by ignoring that maxim.

Berkshire now enjoys $138 billion of insurance “float” – funds that do not belong to us, but are nevertheless ours to deploy, whether in bonds, stocks or cash equivalents such as U.S. Treasury bills. Float has some similarities to bank deposits: cash flows in and out daily to insurers, with the total they hold changing very little. The massive sum held by Berkshire is likely to remain near its present level for many years and, on a cumulative basis, has been costless to us. That happy result, of course, could change – but, over time, I like our odds.

I have repetitiously – some might say endlessly – explained our insurance operation in my annual letters to you. Therefore, I will this year ask new shareholders who wish to learn more about our insurance business and “float” to read the pertinent section of the 2019 report, reprinted on page A-2. It’s important that you understand the risks, as well as the opportunities, existing in our insurance activities.

Our second and third most valuable assets – it’s pretty much a toss-up at this point – are Berkshire’s 100% ownership of BNSF, America’s largest railroad measured by freight volume, and our 5.4% ownership of Apple. And in the fourth spot is our 91% ownership of Berkshire Hathaway Energy (“BHE”). What we have here is a very unusual utility business, whose annual earnings have grown from $122 million to $3.4 billion during our 21 years of ownership.

I’ll have more to say about BNSF and BHE later in this letter. For now, however, I would like to focus on a practice Berkshire will periodically use to enhance your interest in both its “Big Four” as well as the many other assets Berkshire owns.

* * * * * * * * * * * *

Last year we demonstrated our enthusiasm for Berkshire’s spread of properties by repurchasing the equivalent of 80,998 “A” shares, spending $24.7 billion in the process. That action increased your ownership in all of Berkshire’s businesses by 5.2% without requiring you to so much as touch your wallet.

Following criteria Charlie and I have long recommended, we made those purchases because we believed they would both enhance the intrinsic value per share for continuing shareholders and would leave Berkshire with more than ample funds for any opportunities or problems it might encounter.

In no way do we think that Berkshire shares should be repurchased at simply any price. I emphasize that point because American CEOs have an embarrassing record of devoting more company funds to repurchases when prices have risen than when they have tanked. Our approach is exactly the reverse.

Berkshire’s investment in Apple vividly illustrates the power of repurchases. We began buying Apple stock late in 2016 and by early July 2018, owned slightly more than one billion Apple shares (split-adjusted). Saying that, I’m referencing the investment held in Berkshire’s general account and am excluding a very small and separately-managed holding of Apple shares that was subsequently sold. When we finished our purchases in mid-2018, Berkshire’s general account owned 5.2% of Apple.

Our cost for that stake was $36 billion. Since then, we have both enjoyed regular dividends, averaging about $775 million annually, and have also – in 2020 – pocketed an additional $11 billion by selling a small portion of our position.

Despite that sale – voila! – Berkshire now owns 5.4% of Apple. That increase was costless to us, coming about because Apple has continuously repurchased its shares, thereby substantially shrinking the number it now has outstanding.

But that’s far from all of the good news. Because we also repurchased Berkshire shares during the 2 1⁄2 years, you now indirectly own a full 10% more of Apple’s assets and future earnings than you did in July 2018.

This agreeable dynamic continues. Berkshire has repurchased more shares since yearend and is likely to further reduce its share count in the future. Apple has publicly stated an intention to repurchase its shares as well. As these reductions occur, Berkshire shareholders will not only own a greater interest in our insurance group and in BNSF and BHE, but will also find their indirect ownership of Apple increasing as well.

The math of repurchases grinds away slowly, but can be powerful over time. The process offers a simple way for investors to own an ever-expanding portion of exceptional businesses.

And as a sultry Mae West assured us: “Too much of a good thing can be... wonderful.”

Investments

Below we list our fifteen common stock investments that at yearend were our largest in market value. We exclude our Kraft Heinz holding — 325,442,152 shares — because Berkshire is part of a control group and therefore must account for that investment using the “equity” method. On its balance sheet, Berkshire carries the Kraft Heinz

holding at a GAAP figure of $13.3 billion, an amount that represents Berkshire’s share of the audited net worth of Kraft Heinz on December 31, 2020. Please note, though, that the market value of our shares on that date was only $11.3 billion.

A Tale of Two Cities

Success stories abound throughout America. Since our country’s birth, individuals with an idea, ambition and often just a pittance of capital have succeeded beyond their dreams by creating something new or by improving the customer’s experience with something old.

Charlie and I journeyed throughout the nation to join with many of these individuals or their families. On the West Coast, we began the routine in 1972 with our purchase of See’s Candy. A full century ago, Mary See set out to deliver an age-old product that she had reinvented with special recipes. Added to her business plan were quaint stores staffed by friendly salespeople. Her first small outlet in Los Angeles eventually led to several hundred shops, spread throughout the West.

Today, Mrs. See’s creations continue to delight customers while providing life-long employment for thousands of women and men. Berkshire’s job is simply not to meddle with the company’s success. When a business manufactures and distributes a non-essential consumer product, the customer is the boss. And, after 100 years, the customer’s message to Berkshire remains clear: “Don’t mess with my candy.” (The website is https://www.sees.com/; try the peanut brittle.)

Let’s move across the continent to Washington, D.C. In 1936, Leo Goodwin, along with his wife, Lillian, became convinced that auto insurance – a standardized product customarily purchased from agents – could be sold directly at a much lower price. Armed with $100,000, the pair took on giant insurers possessing 1,000 times or more their capital. Government Employees Insurance Company (later shortened to GEICO) was on its way.

By luck, I was exposed to the company’s potential a full 70 years ago. It instantly became my first love (of an investment sort). You know the rest of the story: Berkshire eventually became the 100% owner of GEICO, which at 84 years of age is constantly fine-tuning – but not changing – the vision of Leo and Lillian.

There has been, however, a change in the company’s size. In 1937, its first full year of operation, GEICO did $238,288 of business. Last year the figure was $35 billion.

* * * * * * * * * * * *

Today, with much of finance, media, government and tech located in coastal areas, it’s easy to overlook the many miracles occurring in middle America. Let’s focus on two communities that provide stunning illustrations of the talent and ambition existing throughout our country.

You will not be surprised that I begin with Omaha.

In 1940, Jack Ringwalt, a graduate of Omaha’s Central High School (the alma mater as well of Charlie, my dad, my first wife, our three children and two grandchildren), decided to start a property/casualty insurance company funded by $125,000 in capital.

Jack’s dream was preposterous, requiring his pipsqueak operation – somewhat pompously christened as National Indemnity – to compete with giant insurers, all of which operated with abundant capital. Additionally, those competitors were solidly entrenched with nationwide networks of well-funded and long-established local agents.

Under Jack’s plan, National Indemnity, unlike GEICO, would itself use whatever agencies deigned to accept it and consequently enjoy no cost advantage in its acquisition of business. To overcome those formidable handicaps, National Indemnity focused on “odd-ball” risks, which were deemed unimportant by the “big boys.” And, improbably, the strategy succeeded.

Jack was honest, shrewd, likeable and a bit quirky. In particular, he disliked regulators. When he periodically became annoyed with their supervision, he would feel an urge to sell his company.

Fortunately, I was nearby on one of those occasions. Jack liked the idea of joining Berkshire, and we made a deal in 1967, taking all of 15 minutes to reach a handshake. I never asked for an audit.

Today National Indemnity is the only company in the world prepared to insure certain giant risks. And, yes, it remains based in Omaha, a few miles from Berkshire’s home office.

Over the years, we have purchased four additional businesses from Omaha families, the best known among them being Nebraska Furniture Mart (“NFM”). The company’s founder, Rose Blumkin (“Mrs. B”), arrived in Seattle in 1915 as a Russian emigrant, unable to read or speak English. She settled in Omaha several years later and by 1936 had saved $2,500 with which to start a furniture store.

Competitors and suppliers ignored her, and for a time their judgment seemed correct: World War II stalled her business, and at yearend 1946, the company’s net worth had grown to only $72,264. Cash, both in the till and on deposit, totaled $50 (that’s not a typo).

One invaluable asset, however, went unrecorded in the 1946 figures: Louie Blumkin, Mrs. B’s only son, had rejoined the store after four years in the U.S. Army. Louie fought at Normandy’s Omaha Beach following the D-Day invasion, earned a Purple Heart for injuries sustained in the Battle of the Bulge, and finally sailed home in November 1945.

Once Mrs. B and Louie were reunited, there was no stopping NFM. Driven by their dream, mother and son 0worked days, nights and weekends. The result was a retailing miracle.

By 1983, the pair had created a business worth $60 million. That year, on my birthday, Berkshire purchased 80% of NFM, again without an audit. I counted on Blumkin family members to run the business; the third and fourth generation do so today. Mrs. B, it should be noted, worked daily until she was 103 – a ridiculously premature retirement age as judged by Charlie and me.

NFM now owns the three largest home-furnishings stores in the U.S. Each set a sales record in 2020, a feat achieved despite the closing of NFM’s stores for more than six weeks because of COVID-19.

A post-script to this story says it all: When Mrs. B’s large family gathered for holiday meals, she always asked that they sing a song before eating. Her selection never varied: Irving Berlin’s “God Bless America.”

* * * * * * * * * * * *

Let’s move somewhat east to Knoxville, the third largest city in Tennessee. There, Berkshire has ownership in two remarkable companies – Clayton Homes (100% owned) and Pilot Travel Centers (38% owned now, but headed for 80% in 2023).

Each company was started by a young man who had graduated from the University of Tennessee and stayed put in Knoxville. Neither had a meaningful amount of capital nor wealthy parents.

But, so what? Today, Clayton and Pilot each have annual pre-tax earnings of more than $1 billion. Together they employ about 47,000 men and women.

Jim Clayton, after several other business ventures, founded Clayton Homes on a shoestring in 1956, and “Big Jim” Haslam started what became Pilot Travel Centers in 1958 by purchasing a service station for $6,000. Each of the men later brought into the business a son with the same passion, values and brains as his father. Sometimes there is a magic to genes.

“Big Jim” Haslam, now 90, has recently authored an inspirational book in which he relates how Jim Clayton’s son, Kevin, encouraged the Haslams to sell a large portion of Pilot to Berkshire. Every retailer knows that satisfied customers are a store’s best salespeople. That’s true when businesses are changing hands as well.

* * * * * * * * * * * *

When you next fly over Knoxville or Omaha, tip your hat to the Claytons, Haslams and Blumkins as well as to the army of successful entrepreneurs who populate every part of our country. These builders needed America’s framework for prosperity – a unique experiment when it was crafted in 1789 – to achieve their potential. In turn, America needed citizens like Jim C., Jim H., Mrs. B and Louie to accomplish the miracles our founding fathers sought.

Today, many people forge similar miracles throughout the world, creating a spread of prosperity that benefits all of humanity. In its brief 232 years of existence, however, there has been no incubator for unleashing human potential like America. Despite some severe interruptions, our country’s economic progress has been breathtaking.

Beyond that, we retain our constitutional aspiration of becoming “a more perfect union.” Progress on that front has been slow, uneven and often discouraging. We have, however, moved forward and will continue to do so.

Our unwavering conclusion: Never bet against America.

The Berkshire Partnership

Berkshire is a Delaware corporation, and our directors must follow the state’s laws. Among them is a requirement that board members must act in the best interest of the corporation and its stockholders. Our directors embrace that doctrine.

In addition, of course, Berkshire directors want the company to delight its customers, to develop and reward the talents of its 360,000 associates, to behave honorably with lenders and to be regarded as a good citizen of the many cities and states in which we operate. We value these four important constituencies.

None of these groups, however, have a vote in determining such matters as dividends, strategic direction, CEO selection, or acquisitions and divestitures. Responsibilities like those fall solely on Berkshire’s directors, who must faithfully represent the long-term interests of the corporation and its owners. Beyond legal requirements, Charlie and I feel a special obligation to the many individual shareholders of Berkshire. A bit of personal history may help you to understand our unusual attachment and how it shapes our behavior.

* * * * * * * * * * * *

Before my Berkshire years, I managed money for many individuals through a series of partnerships, the first three of those formed in 1956. As time passed, the use of multiple entities became unwieldy and, in 1962, we amalgamated 12 partnerships into a single unit, Buffett Partnership Ltd. (“BPL”).

By that year, virtually all of my own money, and that of my wife as well, had become invested alongside the funds of my many limited partners. I received no salary or fees. Instead, as the general partner, I was compensated by my limited partners only after they secured returns above an annual threshold of 6%. If returns failed to meet that level, the shortfall was to be carried forward against my share of future profits. (Fortunately, that never happened: Partnership returns always exceeded the 6% “bogey.”) As the years went by, a large part of the resources of my parents, siblings, aunts, uncles, cousins and in-laws became invested in the partnership.

Charlie formed his partnership in 1962 and operated much as I did. Neither of us had any institutional investors, and very few of our partners were financially sophisticated. The people who joined our ventures simply trusted us to treat their money as we treated our own. These individuals – either intuitively or by relying on the advice of friends – correctly concluded that Charlie and I had an extreme aversion to permanent loss of capital and that we would not have accepted their money unless we expected to do reasonably well with it.

I stumbled into business management after BPL acquired control of Berkshire in 1965. Later still, in 1969, we decided to dissolve BPL. After yearend, the partnership distributed, pro-rata, all of its cash along with three stocks, the largest by value being BPL’s 70.5% interest in Berkshire.

Charlie, meanwhile, wound up his operation in 1977. Among the assets he distributed to partners was a major interest in Blue Chip Stamps, a company his partnership, Berkshire and I jointly controlled. Blue Chip was also among the three stocks my partnership had distributed upon its dissolution.

In 1983, Berkshire and Blue Chip merged, thereby expanding Berkshire’s base of registered shareholders from 1,900 to 2,900. Charlie and I wanted everyone – old, new and prospective shareholders – to be on the same page.

Therefore, the 1983 annual report – up front – laid out Berkshire’s “major business principles.” The first principle began: “Although our form is corporate, our attitude is partnership.” That defined our relationship in 1983; it defines it today. Charlie and I – and our directors as well – believe this dictum will serve Berkshire well for many decades to come.

* * * * * * * * * * * *

Ownership of Berkshire now resides in five large “buckets,” one occupied by me as a “founder” of sorts. That bucket is certain to empty as the shares I own are annually distributed to various philanthropies.

Two of the remaining four buckets are filled by institutional investors, each handling other people’s money. That, however, is where the similarity between those buckets ends: Their investing procedures could not be more different.

In one institutional bucket are index funds, a large and mushrooming segment of the investment world. These funds simply mimic the index that they track. The favorite of index investors is the S&P 500, of which Berkshire is a component. Index funds, it should be emphasized, own Berkshire shares simply because they are required to do so.

They are on automatic pilot, buying and selling only for “weighting” purposes.

In the other institutional bucket are professionals who manage their clients’ money, whether those funds belong to wealthy individuals, universities, pensioners or whomever. These professional managers have a mandate to move funds from one investment to another based on their judgment as to valuation and prospects. That is an honorable, though difficult, occupation.

We are happy to work for this “active” group, while they meanwhile search for a better place to deploy the funds of their clientele. Some managers, to be sure, have a long-term focus and trade very infrequently. Others use computers employing algorithms that may direct the purchase or sale of shares in a nano-second. Some professional investors will come and go based upon their macro-economic judgments.

Our fourth bucket consists of individual shareholders who operate in a manner similar to the active institutional managers I’ve just described. These owners, understandably, think of their Berkshire shares as a possible source of funds when they see another investment that excites them. We have no quarrel with that attitude, which is similar to the way we look at some of the equities we own at Berkshire.

All of that said, Charlie and I would be less than human if we did not feel a special kinship with our fifth bucket: the million-plus individual investors who simply trust us to represent their interests, whatever the future may bring. They have joined us with no intent to leave, adopting a mindset similar to that held by our original partners. Indeed, many investors from our partnership years, and/or their descendants, remain substantial owners of Berkshire.

A prototype of those veterans is Stan Truhlsen, a cheerful and generous Omaha ophthalmologist as well as personal friend, who turned 100 on November 13, 2020. In 1959, Stan, along with 10 other young Omaha doctors, formed a partnership with me. The docs creatively labeled their venture Emdee, Ltd. Annually, they joined my wife and me for a celebratory dinner at our home.

When our partnership distributed its Berkshire shares in 1969, all of the doctors kept the stock they received. They may not have known the ins and outs of investing or accounting, but they did know that at Berkshire they would be treated as partners.

Two of Stan’s comrades from Emdee are now in their high-90s and continue to hold Berkshire shares. This group’s startling durability – along with the fact that Charlie and I are 97 and 90, respectively – serves up an interesting question: Could it be that Berkshire ownership fosters longevity?

* * * * * * * * * * * *

Berkshire’s unusual and valued family of individual shareholders may add to your understanding of our reluctance to court Wall Street analysts and institutional investors. We already have the investors we want and don’t think that they, on balance, would be upgraded by replacements.

There are only so many seats – that is, shares outstanding – available for Berkshire ownership. And we very much like the people already occupying them.

Of course, some turnover in “partners” will occur. Charlie and I hope, however, that it will be minimal. Who, after all, seeks rapid turnover in friends, neighbors or marriage?

In 1958, Phil Fisher wrote a superb book on investing. In it, he analogized running a public company to managing a restaurant. If you are seeking diners, he said, you can attract a clientele and prosper featuring either hamburgers served with a Coke or a French cuisine accompanied by exotic wines. But you must not, Fisher warned, capriciously switch from one to the other: Your message to potential customers must be consistent with what they will find upon entering your premises.

At Berkshire, we have been serving hamburgers and Coke for 56 years. We cherish the clientele this fare has attracted.

The tens of millions of other investors and speculators in the United States and elsewhere have a wide variety of equity choices to fit their tastes. They will find CEOs and market gurus with enticing ideas. If they want price targets, managed earnings and “stories,” they will not lack suitors. “Technicians” will confidently instruct them as to what some wiggles on a chart portend for a stock’s next move. The calls for action will never stop.

Many of those investors, I should add, will do quite well. After all, ownership of stocks is very much a “positive-sum” game. Indeed, a patient and level-headed monkey, who constructs a portfolio by throwing 50 darts at a board listing all of the S&P 500, will – over time – enjoy dividends and capital gains, just as long as it never gets tempted to make changes in its original “selections.”

Productive assets such as farms, real estate and, yes, business ownership produce wealth – lots of it. Most owners of such properties will be rewarded. All that’s required is the passage of time, an inner calm, ample diversification and a minimization of transactions and fees. Still, investors must never forget that their expenses are Wall Street’s income. And, unlike my monkey, Wall Streeters do not work for peanuts.

When seats open up at Berkshire – and we hope they are few – we want them to be occupied by newcomers who understand and desire what we offer. After decades of management, Charlie and I remain unable to promise results. We can and do, however, pledge to treat you as partners.

And so, too, will our successors.

A Berkshire Number that May Surprise You

Recently, I learned a fact about our company that I had never suspected: Berkshire owns American-based property, plant and equipment – the sort of assets that make up the “business infrastructure” of our country – with a GAAP valuation exceeding the amount owned by any other U.S. company. Berkshire’s depreciated cost of these domestic “fixed assets” is $154 billion. Next in line on this list is AT&T, with property, plant and equipment of $127 billion.

Our leadership in fixed-asset ownership, I should add, does not, in itself, signal an investment triumph. The best results occur at companies that require minimal assets to conduct high-margin businesses – and offer goods or services that will expand their sales volume with only minor needs for additional capital. We, in fact, own a few of these exceptional businesses, but they are relatively small and, at best, grow slowly.

Asset-heavy companies, however, can be good investments. Indeed, we are delighted with our two giants – BNSF and BHE: In 2011, Berkshire’s first full year of BNSF ownership, the two companies had combined earnings of $4.2 billion. In 2020, a tough year for many businesses, the pair earned $8.3 billion.

BNSF and BHE will require major capital expenditures for decades to come. The good news is that both are likely to deliver appropriate returns on the incremental investment.

Let’s look first at BNSF. Your railroad carries about 15% of all non-local ton-miles (a ton of freight moved one mile) of goods that move in the United States, whether by rail, truck, pipeline, barge or aircraft. By a significant margin, BNSF’s loads top those of any other carrier.

The history of American railroads is fascinating. After 150 years or so of frenzied construction, skullduggery, overbuilding, bankruptcies, reorganizations and mergers, the railroad industry finally emerged a few decades ago as mature and rationalized.

BNSF began operations in 1850 with a 12-mile line in northeastern Illinois. Today, it has 390 antecedents whose railroads have been purchased or merged. The company’s extensive lineage is laid out at http://www.bnsf.com/bnsf-resources/pdf/about-bnsf/History_and_Legacy.pdf.

Berkshire acquired BNSF early in 2010. Since our purchase, the railroad has invested $41 billion in fixed assets, an outlay $20 billion in excess of its depreciation charges. Railroading is an outdoor sport, featuring mile-long trains obliged to reliably operate in both extreme cold and heat, as they all the while encounter every form of terrain from deserts to mountains. Massive flooding periodically occurs. BNSF owns 23,000 miles of track, spread throughout 28 states, and must spend whatever it takes to maximize safety and service throughout its vast system.

Nevertheless, BNSF has paid substantial dividends to Berkshire – $41.8 billion in total. The railroad pays us, however, only what remains after it both fulfills the needs of its business and maintains a cash balance of about $2 billion. This conservative policy allows BNSF to borrow at low rates, independent of any guarantee of its debt by Berkshire.

One further word about BNSF: Last year, Carl Ice, its CEO, and his number two, Katie Farmer, did an extraordinary job in controlling expenses while navigating a significant downturn in business. Despite a 7% decline in the volume of goods carried, the two actually increased BNSF’s profit margin by 2.9 percentage points. Carl, as long planned, retired at yearend and Katie took over as CEO. Your railroad is in good hands.

BHE, unlike BNSF, pays no dividends on its common stock, a highly-unusual practice in the electric-utility industry. That Spartan policy has been the case throughout our 21 years of ownership. Unlike railroads, our country’s electric utilities need a massive makeover in which the ultimate costs will be staggering. The effort will absorb all of BHE’s earnings for decades to come. We welcome the challenge and believe the added investment will be appropriately rewarded.

Let me tell you about one of BHE’s endeavors – its $18 billion commitment to rework and expand a substantial portion of the outdated grid that now transmits electricity throughout the West. BHE began this project in 2006 and expects it to be completed by 2030 – yes, 2030.

The advent of renewable energy made our project a societal necessity. Historically, the coal-based generation of electricity that long prevailed was located close to huge centers of population. The best sites for the new world of wind and solar generation, however, are often in remote areas. When BHE assessed the situation in 2006, it was no secret that a huge investment in western transmission lines had to be made. Very few companies or governmental entities, however, were in a financial position to raise their hand after they tallied the project’s cost.

BHE’s decision to proceed, it should be noted, was based upon its trust in America’s political, economic and judicial systems. Billions of dollars needed to be invested before meaningful revenue would flow. Transmission lines had to cross the borders of states and other jurisdictions, each with its own rules and constituencies. BHE would also need to deal with hundreds of landowners and execute complicated contracts with both the suppliers that generated renewable power and the far-away utilities that would distribute the electricity to their customers. Competing interests and defenders of the old order, along with unrealistic visionaries desiring an instantly-new world, had to be brought on board.

Both surprises and delays were certain. Equally certain, however, was the fact that BHE had the managerial talent, the institutional commitment and the financial wherewithal to fulfill its promises. Though it will be many years before our western transmission project is completed, we are today searching for other projects of similar size to take on.

Whatever the obstacles, BHE will be a leader in delivering ever-cleaner energy.

The Annual Meeting

Last year, on February 22nd, I wrote you about our plans for a gala annual meeting. Within a month, the schedule was junked.

Our home office group, led by Melissa Shapiro and Marc Hamburg, Berkshire’s CFO, quickly regrouped. Miraculously, their improvisations worked. Greg Abel, one of Berkshire’s Vice Chairmen, joined me on stage facing a dark arena, 18,000 empty seats and a camera. There was no rehearsal: Greg and I arrived about 45 minutes before “showtime.”

Debbie Bosanek, my incredible assistant who joined Berkshire 47 years ago at age 17, had put together about 25 slides displaying various facts and figures that I had assembled at home. An anonymous but highly-capable team of computer and camera operators projected the slides onto the screen in proper order.

Yahoo streamed the proceedings to a record-sized international audience. Becky Quick of CNBC, operating from her home in New Jersey, selected questions from thousands that shareholders had earlier submitted or that viewers had emailed to her during the four hours Greg and I were on stage. See’s peanut brittle and fudge, along with Coca-Cola, provided us with nourishment.

This year, on May 1st, we are planning to go one better. Again, we will rely on Yahoo and CNBC to perform flawlessly. Yahoo will go live at 1 p.m. Eastern Daylight Time (“EDT”). Simply navigate to https://finance.yahoo.com/brklivestream.

Our formal meeting will commence at 5:00 p.m. EDT and should finish by 5:30 p.m. Earlier, between 1:30-5:00, we will answer your questions as relayed by Becky. As always, we will have no foreknowledge as to what questions will be asked. Send your zingers to [email protected]. Yahoo will wrap things up after 5:30.

And now – drum roll, please – a surprise. This year our meeting will be held in Los Angeles... and Charlie will be on stage with me offering answers and observations throughout the 3 1⁄2-hour question period. I missed him last year and, more important, you clearly missed him. Our other invaluable vice-chairmen, Ajit Jain and Greg Abel, will be with us to answer questions relating to their domains.

Join us via Yahoo. Direct your really tough questions to Charlie! We will have fun, and we hope you will as well.

Better yet, of course, will be the day when we see you face to face. I hope and expect that will be in 2022.

The citizens of Omaha, our exhibiting subsidiaries and all of us at the home office can’t wait to get you back for an honest-to-God annual meeting, Berkshire-style

Warren E. Buffett

Chairman of the Board

February 27, 2021