The past month has been one of the most impactful periods we have experienced since our inception in 2003 — and yes, we have been around longer than many multinational wealth management firms. The ASX 200 declined 6.5% this month, broadly in line with US markets. A key driver of this volatility is the rising cost of energy, which is now flowing through the entire supply chain and into the price of nearly everything. A prolonged closure of the Strait of Hormuz would almost certainly drive inflation higher, placing further pressure on central banks, including the RBA, to continue raising interest rates. However, it is important to recognise interest rate policy primarily impacts demand — not supply — and therefore has limited ability to address energy driven inflation.

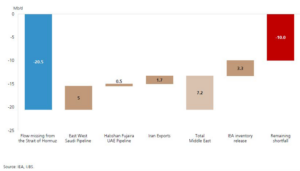

The global energy market is currently undersupplied by approximately 10 million barrels per day.

Rising living costs are eroding savings at a rapid pace, as illustrated by the sharp decline in the US personal savings rate.

US Personal Savings Rate

Source: Macrobond, Bloomberg UBS.

This is particularly important given that the US accounts for nearly 30% of global GDP, with consumer spending driving approximately 70% of its economy. Any sustained weakness in US consumer spending has significant global implications — especially when considering the additional inflationary pressures from potential tariffs. At the same time, the exponential growth of AI is yet to be fully reflected in economic data. While it promises meaningful efficiency gains, it also introduces uncertainty around employment and earnings across several sectors.

We have observed a notable slowdown in residential real estate activity in recent weeks, in Australia and offshore. This is significant, as housing turnover is closely linked to consumer spending and broader economic momentum. In private markets — both private equity and private credit — liquidity is becoming a growing concern. Redemption requests are increasingly exceeding available liquidity, effectively stalling what has been a period of rapid growth in the sector. A particular area of risk lies within private credit funds heavily exposed to software businesses. As AI continues to disrupt traditional software models, earnings pressure is emerging. In many cases, these businesses lack hard assets, leaving creditors exposed in downside scenarios. The movement in gold & silver is also notable.

Source: goldprice.com

Markets are increasingly favouring companies with tangible assets, strong balance sheets, and defensive earnings, over high-growth, speculative businesses. This aligns closely with our longstanding investment philosophy. We focus on acquiring high-quality businesses with proven earnings, strong market positions, and resilient margins. Capital preservation remains central to our approach.