During the month, the All Ordinaries index fell about 2.5%. Considering many stocks are trading ex-dividend, the market has been fairly stable.

ASX 200 chart (1-month)

The US market was down about 0.95% over the same period. Taking such a short-term snapshot of the market can be problematic. A longer-term view is far more constructive and financially rewarding.

The market continues to reach new record highs as it has throughout history, with intermittent periods of short-term volatility:

ASX 200 Accumulation Index (20-year) – including GFC and Covid

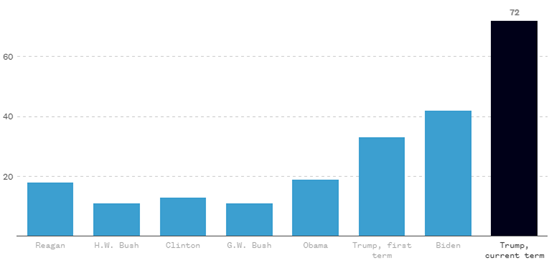

The market appears relatively immune to the frequent announcements from the Trump administration, and the plethora of executive orders being signed. In fact, Trump signed more executive orders in his first 10 days than any recent president has in their first 100 days.

Executive orders in the first 100 days

In the interest of retaining a level of mental wellbeing, investors are best served focusing on company fundamentals. This is important, as previously the market was prone to distractions arising from issues that cannot easily be controlled (e.g.: macroeconomic factors, Trump).

The US economy accounts for 26% of global GDP, with China being the next largest contributor at 17% and then Germany at 4%. Australia has the 13th largest economy contributing nearly 2%, which sounds relatively small but is significant when comparing economies outside the US and China.

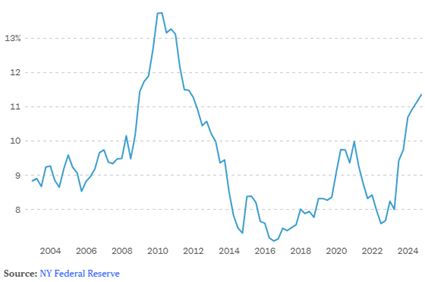

The US consumer is very important, contributing 70% of total US economic activity. Reports around the strength of the US consumer are mixed, with economic growth increasingly powered by the wealthy. Whilst unemployment is historically low and inflation relatively stable, the share of credit card balances 90+ days overdue is at its highest level since 2011, reflecting financial pressure on borrowers.

Credit card delinquencies rising (USA)

Overall, spending in the US is anticipated to grow about 2% p.a. making the decision by the Fed Reserve to drop rates a difficult one. The Australian economy tends to follow the US, as witnessed by similarly strong employment and a more sustainable inflation reading, influencing the RBA decision to drop rates.

We have mentioned in previous newsletters the rate at which money is being printed is creating inflation not only in the price of goods and services (CPI) but more so in asset prices (US & Aust markets near record highs, property near record highs). The amount of cash sitting in bank accounts is at record levels, awaiting a pull-back to be deployed.

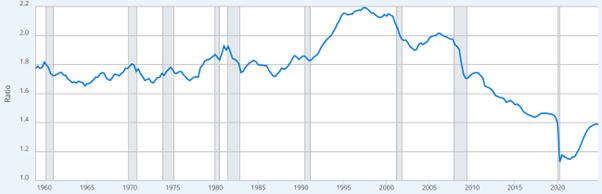

Velocity of Money (M2 Money Stock)

This is the measure of the number of times one dollar is spent to buy goods and services per unit of time. A high velocity of money indicates a bustling economy with strong economic activity, while a low velocity indicates a general reluctance to spend money.

Source: Federal Reserve Bank

Inflation is a combination of any number of factors, including the velocity of money. Whilst more currency is being printed, the rate at which those dollars are distributed in the economy has dropped.

ASX Reporting Season

ASX listed companies are currently reporting 1H FY25 numbers. Overall, a larger number of companies have beaten expectations versus those that have not. A key reason for this is that the economy has performed better than expected in the past six months.

Alex Leyland

Alex.leyland@leyland.com.au